A capital loss arises when a company’s equity (share capital plus legal and free reserves) is no longer fully covered by its assets — that is, when accumulated losses have eroded the company’s capital base to such an extent that liabilities exceed or threaten to exceed available equity. Depending on the severity, this may constitute a capital loss (Unterbilanz) or even overindebtedness (Überschuldung) under Swiss law.

For a Swiss stock corporation (Aktiengesellschaft, AG) in such a situation, the declarative capital reduction introduced by Art. 653p of the Swiss Code of Obligations (CO) provides an important statutory instrument for balance sheet restructuring.

It enables a formal balance sheet adjustment that restores capital adequacy without any outflow of funds and without triggering the creditor protection procedures applicable to an ordinary capital reduction.

Legal Basis — Art. 653p CO

As part of the comprehensive Swiss corporate law reform that entered into force on 1 January 2023, the legislator introduced Art. 653p CO. The provision governs the reduction of share capital for the purpose of offsetting losses, under specific conditions verified by an independent audit expert.

In simplified terms, the article provides:

Where the share capital is reduced to eliminate a loss and a licensed audit expert confirms to the general meeting that the reduction does not exceed the amount of the loss, certain requirements applicable to ordinary capital reductions — such as the obligation to prepare an interim balance sheet and to secure creditors’ claims — shall not apply.

The general meeting’s resolution must meet the formal requirements of Art. 653n CO and must include a corresponding amendment to the articles of association.

The key distinction lies in the absence of a capital outflow: the reduction is purely declarative (book-based), serving to align the nominal share capital with the company’s actual net assets.

Consequently, the procedure is faster, less formal, and more cost-efficient, while maintaining creditor protection, as the transaction does not adversely affect the company’s asset position.

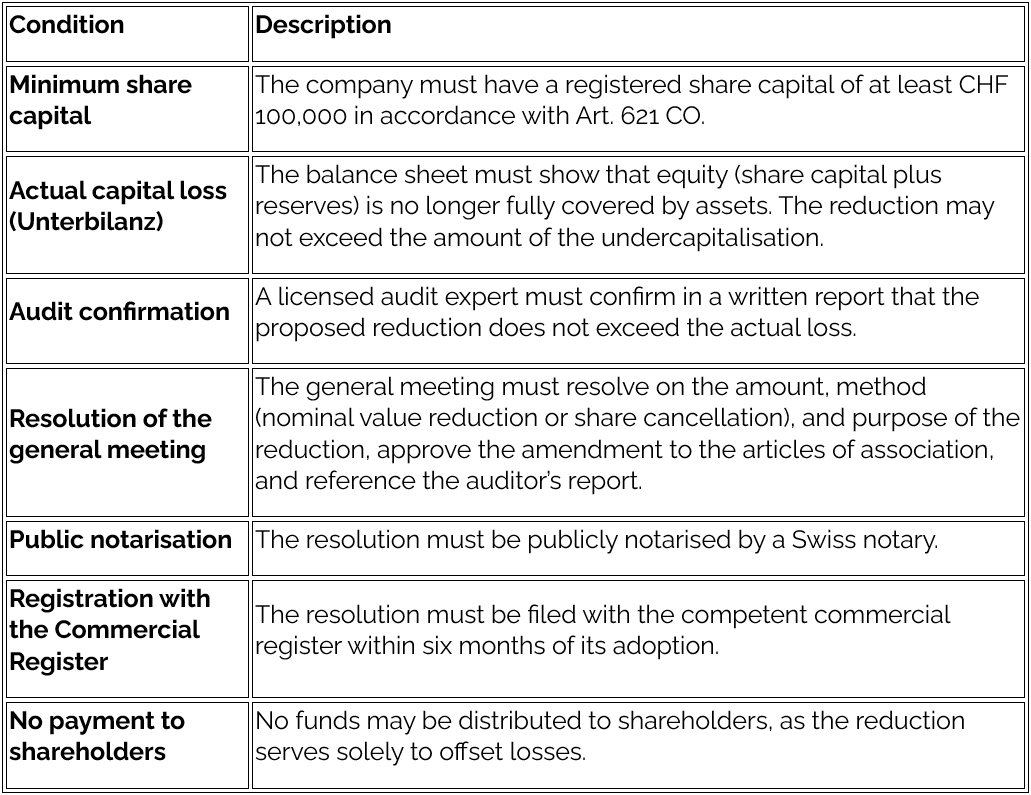

Requirements and Limitations

To validly implement a declarative capital reduction, the following conditions must be satisfied:

Procedural Steps

- Determination of the capital loss

The company prepares annual or interim financial statements evidencing the extent of the undercapitalisation. - Audit report

A licensed audit expert verifies and confirms that the proposed reduction amount does not exceed the actual loss. - Preparation of the general meeting

The board of directors convenes a general meeting and proposes:

- the amount and form of the reduction;

- its purpose (offsetting the loss);

- the amendment to the articles of association; and

- reference to the auditor’s confirmation. - General meeting and notarisation

The resolution is passed by the general meeting and publicly notarised by a notary. - Filing with the Commercial Register

The notarised documents are filed with the Commercial Register within six months. - Registration and publication

Upon examination, the commercial register records the reduction and publishes it in the Swiss Official Gazette of Commerce (SHAB). - Accounting implementation

The company adjusts its balance sheet, eliminates the accumulated losses, and updates the share register and statutory accounts accordingly. - Restoration of distributable profits

Following registration, the company’s equity is restored, and the corporation becomes eligible to declare dividends again, provided other legal requirements are satisfied.

Advantages

- Restores distributable equity by eliminating accumulated losses.

- No liquidity impact, as no payments are made to shareholders.

- Streamlined procedure — creditor protection measures are not required.

- Improved balance sheet presentation enhances transparency and creditworthiness.

- Efficient and cost-effective compared to ordinary capital reductions.

Risks and Common Pitfalls

- Deficient audit report — without a compliant confirmation, the resolution may be voidable.

- Missed filing deadline — if the resolution is not filed within six months, it lapses automatically.

- Incorrect amendment to articles — errors in capital figures or nominal values can delay registration.

- Minority shareholder challenges — dissenting shareholders may seek to contest the decision.

- Tax implications — adjustments may affect deferred taxes or reserves; early tax advice is recommended.

- Interaction with capital band provisions — reductions must respect any capital band limits recorded in the articles of association.

Conclusion

The declarative capital reduction under Art. 653p CO is one of the most pragmatic and effective corporate restructuring instruments available under Swiss law.

It enables a company to restore balance sheet integrity, eliminate historical losses, and regain dividend capacity — all without capital inflows, without creditor protection procedures, and with minimal administrative effort.

For any company facing undercapitalisation, early consultation with a licensed audit expert and a notary public is strongly recommended. With proper preparation, the entire process can be completed within a matter of weeks — leaving the corporation on a sound and compliant financial footing.