Employee participation plans – whether equity-based or virtual – are a popular instrument to motivate employees, retain them in the company and allow them to participate in the economic success of the business. In particular, SMEs and start-ups use such participation plans to retain key talent and management in the long term and to implement succession planning.

At first glance, this seems like a win-win situation for both the employee and the employer. Employees who receive shares or options can benefit from increases in value, while the employer strengthens employee loyalty. However, granting employee participation at preferential conditions can have adverse tax consequences

The tax treatment and structuring of employee equity plans should not be underestimated; it varies by canton and entails risks. Pitfalls can arise both in valuing the employee equity and in any potential capital gain. We’ll set out the fundamentals and explain the biggest tax traps.

1. Non-equity employee participations: concept and tax classification

Non-equity employee participations are not actual equity interests in the employer; in other words, they are not equity-based awards. Rather, they take the form of virtual or phantom shares granted to employees. In substance, such virtual shares are nothing more than a cash settlement. As a rule, virtual shares are structured so that eligible employees receive compensation when the actual shareholders receive dividends or when the company is sold. Non-equity employee participations do not confer voting rights or other proprietary rights that accompany an ordinary share or a capital contribution.

The grant or acquisition of non-equity employee participations by an employee does not trigger tax consequences, because at that stage it is merely a contingent entitlement. Only upon receipt – i.e., when the cash is paid out – must the employee tax the entire amount as income from employment (so-called back-end taxation). Until a payout occurs, such instruments are not subject to wealth tax. In addition, the usual social security contributions are due upon payout. Finally, non-equity employee participations do not give rise to tax-free capital gains.

2. Equity-based employee participations: definition

By contrast, equity-based employee participations represent an ownership interest in the employer’s equity. Employees receive shares, capital contributions, participation certificates or options in the company, together with the governance and economic rights that attach to them. As a rule, such equity-based participations are issued to employees on preferential terms.

3. The tax classification of equity-based employee participations

Equity-based employee participations are taxable at the time of acquisition as income from employment (so-called front-end taxation). The employee must tax the difference between the fair market value of the instruments and the acquisition price – that is, the discount. Fair market value is the price an independent third party would pay under normal market conditions. The decisive parameters for the tax return are therefore the fair market value and the purchase price of the employee participation received. Equity-based employee participations are also subject to wealth tax; the foregoing applies mutatis mutandis. In addition, the usual social security contributions are due on such participations.

Fair market value and formula value

If the equity-based participations are shares in a listed employer, the fair market value is the closing price of the relevant share on the acquisition date.

For (non-listed) SMEs, there is typically no readily ascertainable market value. In the absence of a market price, other valuation methods are used. The fair market value in non-listed companies is thus determined by an equivalent formula value. This formula value must be calculated using an “appropriate and recognised method.” The company may apply a method suitable for it – for example, the widely used practitioner method (Praktikermethode); however, the Canton of Zurich does not regard the discounted cash flow (DCF) method as appropriate. The company must stick to the valuation method once chosen for its employee participation plan and perform a separate valuation for each share class (e.g., common shares and preference shares).

If an employee acquires equity-based participations at the formula value, the acquisition does not trigger income tax. If, however, the participations are acquired below the formula value – i.e., on preferential terms – the difference between the purchase price and the formula value must be taxed at the time of acquisition as income from employment.

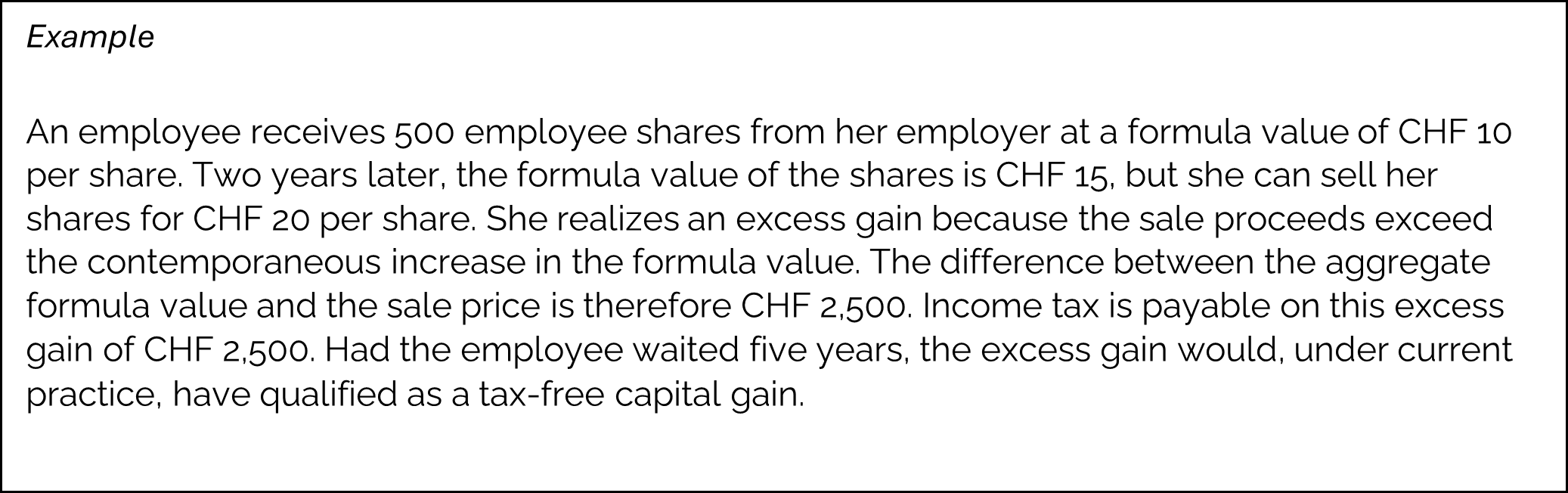

Excess-gain taxation or tax-free capital gain

Because valuation is based on the formula value, the formula-value principle (Formelwertprinzip) applies: a tax-free capital gain upon disposal of the participations is only possible to the extent of the increase in the formula value itself. If, upon disposal (e.g., at an exit), a gain is realised that exceeds the increase in the formula value, this is an excess gain (Übergewinn). If such a disposal occurs within five years after acquisition, income tax is levied on the excess gain (so-called excess-gain taxation, Übergewinnbesteuerung). Only after five years does the excess gain qualify as a tax-free capital gain on equity-based employee participations.

What applies if, exceptionally, a fair market value exists?

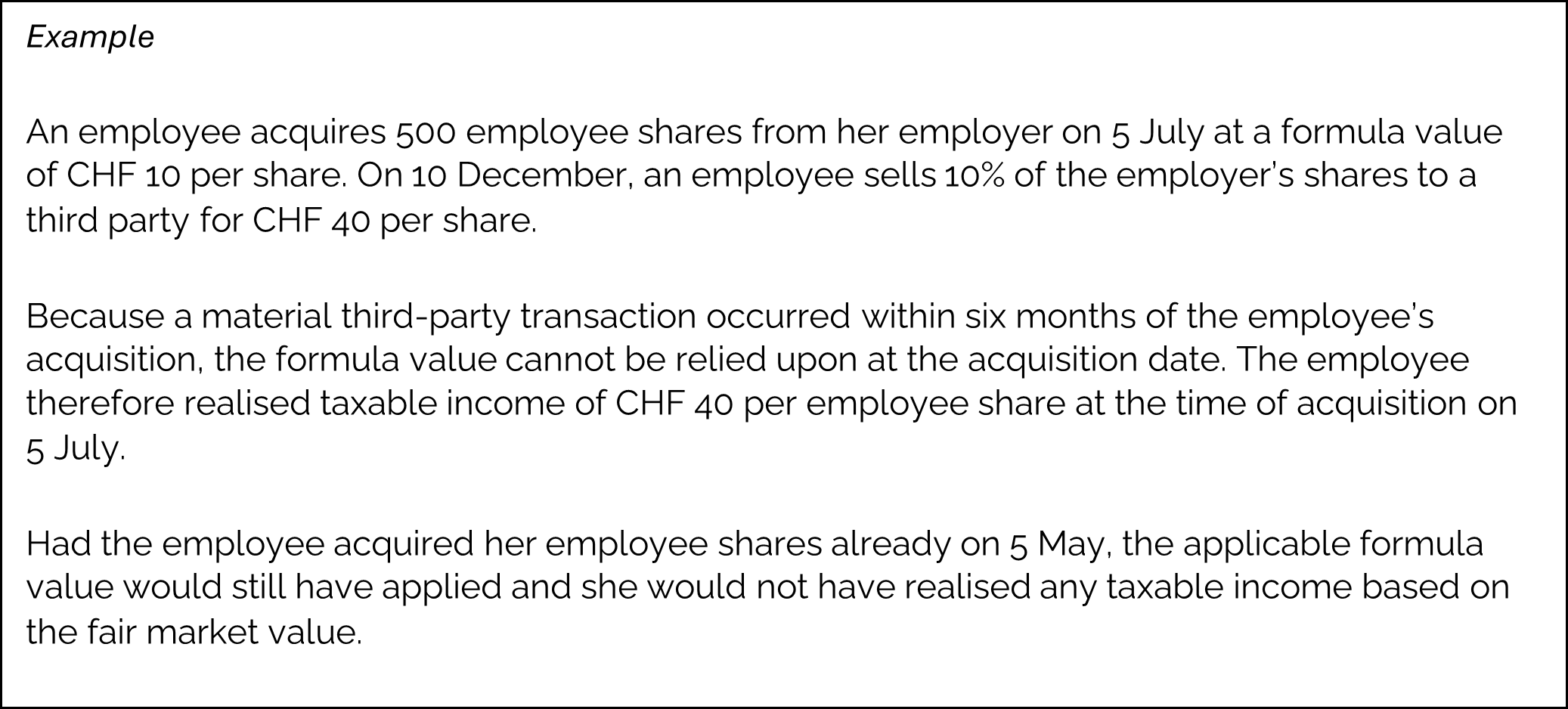

If, in exceptional cases, a fair market value is available for participations in non-listed companies, that fair market value is, in principle, decisive for tax purposes. If an employee then acquires the employee participations at a formula value that is lower than the existing fair market value, this triggers income tax consequences.

A fair market value is only available if a third-party transaction has taken place. That transaction must be timely and quantitatively significant. Under the practice in the Canton of Zurich, the third-party transaction must have occurred within six months before or after the acquisition of the employee participations. The fair market value applies even if, at the time of acquisition, no third-party transaction could have been anticipated. A transaction is considered quantitatively significant – i.e., determinative – if the transaction volume is at least 10%. In that case, the taxable amount is the difference between the acquisition price determined under the formula value and the fair market value.

If the third-party transaction results in income tax being due on the acquisition of employee participations, those participations will thereafter be subject to the fair-market-value principle and no longer to the formula-value principle.

If a company conducts a financing round (i.e., a capital increase), the price paid for the shares – provided the 10% threshold is met – also constitutes a material third-party price. However, if a start-up that qualifies as a “start-up company” under the directive of the Zurich Department of Finance (Finanzdirektion des Kantons Zürich) carries out a financing round, the purchase price paid in that round may be disregarded.

4. Pitfalls

Lock-up periods and vesting

Employee participation plans often provide that employees cannot dispose of their awards immediately. During the vesting period (Sperrfrist), the employee “earns” the participations over time. Once the vesting period ends, the participations are deemed vested and the employee acquires a legal claim to them. Vesting affects taxation.

For equity-based participations, vesting is taken into account when calculating the taxable benefit by applying a 6% discount per lock-up year to the fair market or formula value, for a maximum of ten years.

For non-equity participations, there is no discount, because they are taxed only upon receipt and the amounts paid out are no longer subject to vesting.

Founders’ shares and investors’ shares

A fine but important distinction: equity-based employee participations must be distinguished from (i) participations acquired at the time of formation (founders’ shares, Gründeraktien) and (ii) participations granted on market terms. From a tax perspective, the subsequent disposal of such shares generally results in a tax-free capital gain. If a person received their participations in their capacity as founder – not as an employee – the benefit is not classified as employment income.

Likewise, if an investor acquires participations as part of an investment, these are not employee participations, as the acquisition is unrelated to an employment relationship; the disposal of such participations also does not trigger excess-gain taxation.

This distinction is particularly important for young companies and start-ups: whereas employees face a risk of income-tax consequences on their employee participations, founders can generally sell their participations tax-free.

Management buyouts and succession planning

Acquisitions of participations in the context of a corporate succession arrangement also constitute acquisitions of employee participations if the acquisition is causally linked to an existing or future employment relationship.

Earn-outs or milestone payments

When a start-up or SME is sold, the purchase price often consists of a fixed amount plus earn-outs or milestone payments payable upon meeting performance targets or milestones. If the current seller originally acquired their participations at fair market value, the amounts received in the new transaction constitute tax-free capital gains. If, however, the participations were originally acquired at the formula value, only the portion of the proceeds up to the formula value at the time of the transaction is tax-free; any amount above that formula value is taxable income, regardless of whether it forms part of the fixed price or the performance-based component. The five-year rule still applies: if the performance-based components become due more than five years after the transaction, they too are tax-free capital gains.

Employee options

An option grants the employee the right, within a defined period and at a specified price, to acquire shares or quota interests in the employer. For income-tax purposes, options are recognised upon exercise, i.e., when they are converted into shares or quota interests.

Employee participations in foreign currency

If the employee participation is denominated in a foreign currency, it must be converted into Swiss francs. For the conversion, use the average (mid-rate) of the closing bid and ask rates on the date of the actual acquisition of the participation.

Ruling

It is often advisable to obtain an advance tax ruling from the competent tax authority for (equity-based) employee participations. This helps ensure uniform assessment of employees and a correct, consistent handling of participation plans in inter-cantonal and international situations.

Reporting/certification requirement

The Employee Participation Ordinance (Mitarbeiterbeteiligungsverordnung, MBV) sets out what information employers must certify to the tax authorities – both upon grant and upon realisation of the taxable benefit – and applies to both equity-based and non-equity participations.

In particular, the MBV certificate must include the name of the plan, the date of acquisition, the number of participations acquired, and the fair market or formula value at the acquisition date.

5. Conclusion

Employee participation plans are a powerful tool for Swiss SMEs and start-ups – but they only pay off legally and tax-wise if the fundamentals are right. What matters most is: clean structuring (equity vs. non-equity plans), a transparent and suitable valuation method (formula value vs. fair market value), proper consideration of vesting, and excess-gain taxation (the five-year rule). At exit, earn-outs or milestone payments must be structured correctly; an advance tax ruling provides legal certainty.

Our tip: fix and clearly document the valuation method, obtain a ruling, and review each transaction in advance. This helps avoid tax pitfalls and capture the full value of employee equity.

Beyond tax issues, employee participations can also raise corporate and employment-law questions. It’s worth addressing these early. We can support you end-to-end – legally , tax-wise, and strategically – so you can implement your employee participation plan successfully.